All Categories

Featured

Table of Contents

These features can vary from company-to-company, so be certain to discover your annuity's fatality benefit features. There are several advantages. 1. A MYGA can mean reduced tax obligations than a CD. With a CD, the interest you earn is taxed when you make it, despite the fact that you do not get it until the CD matures.

So at the really least, you pay tax obligations later, instead than sooner. Not only that, yet the worsening passion will be based on an amount that has not already been exhausted. 2. Your beneficiaries will get the full account value since the day you dieand no abandonment fees will be subtracted.

Your recipients can select either to receive the payout in a round figure, or in a series of income settlements. 3. Frequently, when someone passes away, also if he left a will, a court determines who obtains what from the estate as sometimes relatives will argue regarding what the will means.

With a multi-year set annuity, the owner has plainly assigned a recipient, so no probate is needed. If you contribute to an Individual retirement account or a 401(k) plan, you obtain tax obligation deferment on the revenues, simply like a MYGA.

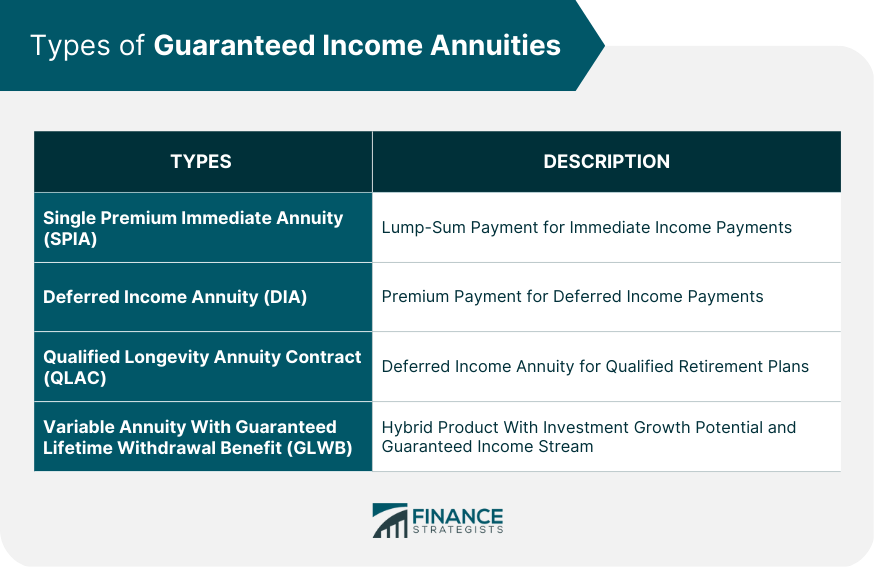

Immediate Life Annuity

Those products already provide tax obligation deferment. MYGAs are wonderful for individuals who want to stay clear of the threats of market fluctuations, and want a taken care of return and tax deferment.

When you pick one, the rates of interest will be repaired and ensured for the term you select. The insurer spends it, generally in high quality lasting bonds, to fund your future settlements under the annuity. That's due to the fact that bonds are quite risk-free. But they can likewise purchase stocks. Remember, the insurance firm is depending not just on your specific settlement to fund your annuity.

These payments are constructed right into the acquisition cost, so there are no covert costs in the MYGA contract. As a matter of fact, deferred annuities do not bill fees of any type of kind, or sales costs either. Certain. In the current environment of low rate of interest, some MYGA investors build "ladders." That indicates buying several annuities with staggered terms.

Guaranteed Period

If you opened up MYGAs of 3-, 4-, 5- and 6-year terms, you would have an account growing each year after three years (pros and cons of purchasing an annuity). At the end of the term, your cash might be withdrawn or taken into a new annuity-- with good luck, at a greater price. You can additionally use MYGAs in ladders with fixed-indexed annuities, a strategy that seeks to make best use of yield while also shielding principal

As you contrast and contrast images supplied by numerous insurance provider, take into account each of the locations detailed over when making your decision. Understanding agreement terms in addition to each annuity's benefits and negative aspects will certainly enable you to make the ideal decision for your financial scenario. Think meticulously about the term.

Annuities 101 How To Sell To Senior Citizens

If passion prices have actually increased, you might desire to secure them in for a longer term. Throughout this time, you can get all of your cash back.

The business you acquire your multi-year guaranteed annuity via accepts pay you a fixed rates of interest on your premium quantity for your chosen amount of time. You'll get rate of interest attributed regularly, and at the end of the term, you either can renew your annuity at an updated rate, leave the money at a taken care of account rate, choose a negotiation choice, or withdraw your funds.

Can You Buy Annuity Without Pension

Since a MYGA supplies a set rates of interest that's assured for the contract's term, it can provide you with a foreseeable return. Protection from market volatility. With prices that are set by agreement for a specific number of years, MYGAs aren't subject to market changes like other investments. Tax-deferred development.

Limited liquidity. Annuities usually have penalties for early withdrawal or surrender, which can restrict your capacity to access your cash without costs. Reduced returns than other financial investments. MYGAs might have reduced returns than stocks or shared funds, which might have greater returns over the long-term. Charges and costs. Annuities usually have abandonment fees and administrative expenses.

MVA is an adjustmenteither positive or negativeto the built up value if you make a partial abandonment over the cost-free amount or completely surrender your contract during the surrender charge duration. Inflation risk. Due to the fact that MYGAs offer a fixed price of return, they may not maintain pace with rising cost of living over time. Not insured by FDIC.

Annuity Accumulation Phase

MYGA prices can alter frequently based on the economic situation, yet they're usually greater than what you would certainly make on a cost savings account. Required a refresher course on the 4 basic kinds of annuities? Find out a lot more how annuities can ensure an earnings in retirement that you can not outlast.

If your MYGA has market worth adjustment arrangement and you make a withdrawal prior to the term mores than, the firm can change the MYGA's surrender worth based upon adjustments in rate of interest prices - can i cancel my annuity. If prices have raised given that you purchased the annuity, your surrender value might decrease to account for the greater rate of interest atmosphere

However, annuities with an ROP provision normally have reduced guaranteed passion prices to counter the firm's potential risk of having to return the costs. Not all MYGAs have an MVA or an ROP. Terms rely on the company and the agreement. At the end of the MYGA period you've chosen, you have three alternatives: If having a guaranteed rate of interest rate for a set number of years still lines up with your monetary method, you just can renew for an additional MYGA term, either the same or a different one (if offered).

With some MYGAs, if you're not exactly sure what to do with the cash at the term's end, you don't need to do anything. The built up worth of your MYGA will certainly move into a fixed account with an eco-friendly one-year rates of interest identified by the company - deferred annuities calculator. You can leave it there up until you determine on your next action

While both deal assured prices of return, MYGAs commonly offer a greater passion price than CDs. MYGAs expand tax obligation deferred while CDs are strained as revenue yearly.

With MYGAs, abandonment fees may use, depending on the type of MYGA you pick. You may not only shed rate of interest, however additionally principalthe money you initially added to the MYGA.

Is Annuity A Good Retirement Option

This means you may shed rate of interest however not the primary quantity added to the CD.Their conventional nature usually allures a lot more to individuals that are approaching or currently in retired life. They might not be ideal for everyone. A might be ideal for you if you intend to: Make the most of a guaranteed rate and lock it in for an amount of time.

Take advantage of tax-deferred profits development. Have the option to choose a settlement alternative for a guaranteed stream of revenue that can last as long as you live. As with any kind of kind of savings automobile, it is essential to thoroughly review the terms of the item and talk to to figure out if it's a wise choice for achieving your specific requirements and objectives.

1All warranties including the death advantage payments are reliant upon the insurance claims paying capability of the releasing company and do not put on the investment efficiency of the hidden funds in the variable annuity. Properties in the hidden funds undergo market threats and might vary in value. Variable annuities and their hidden variable investment choices are offered by syllabus only.

What Is A Lifetime Income Annuity

This and other info are included in the prospectus or recap program, if offered, which may be acquired from your investment expert. Please read it prior to you spend or send money. 2 Ratings are subject to transform and do not put on the underlying investment alternatives of variable products. 3 Present tax regulation undergoes interpretation and legal modification.

Entities or individuals distributing this details are not accredited to provide tax obligation or legal recommendations. Individuals are motivated to look for specific recommendations from their personal tax obligation or lawful guidance. 4 , Exactly How Much Do Annuities Pay? 2023This product is planned for basic public usage. By providing this content, The Guardian Life Insurance Policy Business of America, The Guardian Insurance Policy & Annuity Company, Inc .

{kind=link}

Table of Contents

Latest Posts

Exploring Annuity Fixed Vs Variable Key Insights on Choosing Between Fixed Annuity And Variable Annuity What Is Tax Benefits Of Fixed Vs Variable Annuities? Advantages and Disadvantages of What Is Var

Breaking Down Your Investment Choices A Closer Look at Variable Annuity Vs Fixed Indexed Annuity Defining Fixed Annuity Or Variable Annuity Pros and Cons of Various Financial Options Why Choosing the

Analyzing Variable Annuity Vs Fixed Annuity A Comprehensive Guide to Investment Choices What Is Variable Annuity Vs Fixed Indexed Annuity? Benefits of Choosing the Right Financial Plan Why Choosing th

More

Latest Posts